“Financial planners are nothing but product salespeople that can’t be trusted. I don’t need their help to retire!”

Unfortunately, not an uncommon refrain, I suspect every financial planner has heard something along these lines in the last couple of years.

Which is a shame because today’s financial planner is streets ahead of the old stereotype. We’re not just here to help people with their investments, super and a bit of insurance. Our value is no longer defined by how much product we sell, but by the difference our advice makes in people’s lives.

That value can be tangible, but the most powerful aspects of our work come from the intangible:

-

The feeling that somebody knows your entire financial picture.

-

The confidence that comes from knowing that each element of your finances are in top shape.

-

The moment when you’re about to lose some sleep, worrying about your finances only to realise that there’s nothing to worry about anymore.

-

The certainty that comes with having a clear, documented plan that you’re being held accountable to.

-

These benefits can’t be shown in a balance sheet but they make a world of difference.

This is doubly true when it comes to planning for your retirement.

Good financial advice, at the right time, can be the difference between a crummy retirement – and a relaxed one.

But, hey, it’s easy to talk in vague terms about how a financial planner can help you retire – what’s that actually mean?

The 3 Phases of Retirement

There are a lot of ways we can help, but it might be most useful to consider our role in the three phases of your retirement planning.

(Now, this structure assumes that you’ve done the right things for the bulk of your working life – lived within your means, put money into super when possible, paid down debt, invested a little bit here and there. In other words, you’ve already laid the foundation. If that’s not the case, then I believe our role should start much earlier – as soon as you’re ready to, really.)

There are three distinct phases when it comes to retirement:

-

Planning

-

Jumping

-

Landing

And a financial planner can be incredibly helpful in each phase.

-

Planning

This phase should really start as early as possible, but at least 5-8 years out from your retirement. If you’re retiring at 65, then, I believe you’d want to be actively planning by the time you turn 57, at least.

This gives you time to get everything in order and fix up any issues or mistakes. It’s also long enough that you can see some benefit from letting early improvements compound.

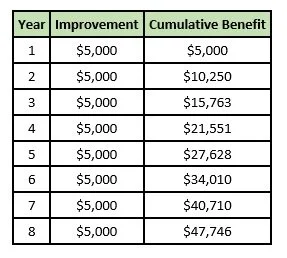

In fact, as a demonstration of this, the following table captures the potential impact of small changes.

Assume that we’re able to find $5,000 of improvements in your financial situation (fee savings, interest reductions, budgeting improvements – things besides ‘better returns’, which we’ve fixed at 5% a year).

And this improvement is a permanent benefit, every year until you retire:

That’s nearly $50,000 in benefits that’s added to your financial position come retirement, by taking small, consistent and achievable steps.

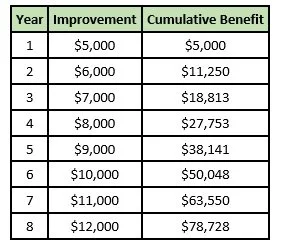

We can play with this calculation a bit too – say we can improve the improvements by an extra $1,000 a year:

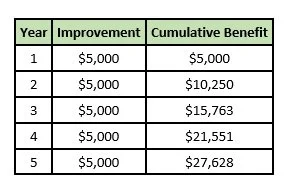

But also, say you don’t start the process until a bit closer to retirement:

In finance, mathematical reality tends to mean that the impact of your habits are exponentially linked to how long you’re doing them. Just three extra years of planning here means another $20,000 in your retirement fund.

The Plan

Now this little traipse down mathematics lane is just to show you one small part of how working with a financial planner can help you build the best retirement possible.

And all of it comes down to ‘The Plan’.

Like any plan, your retirement plan should incorporate:

-

Objectives

-

An understanding of the challenges to overcome

-

Strategies to marshal your resources towards achieving the objectives

-

Landmarks and milestones to measure progress

All of which a planner can help you identify, articulate and document.

If nothing else, I’m fairly sure we’re the only people that’ll ever ask you – “what does retirement mean for you?”.

How We Can Help

What does this look like in reality though? Well, here are some of the specific things we can do to help:

-

Work out the path you’re currently on

We all have a current financial trajectory – a path we’re currently walking into the future. A financial planner will work out that trajectory for you and answer the most important question you have in this phase – “am I on track?”.

-

Technical expertise

Us planners are guilty of not always appreciating just how complex the retirement landscape is.

We do it every day, so we take for granted an understanding of the transition to retirement rules, or the power of salary sacrifice, or contribution timing strategies, or sequencing risk mitigation, or any number of other arcane complexities that every retiree needs to deal with on their way to farewelling work for the last time.

-

Show you how to improve things

Taking these first two areas, we can recommend steps you can take – now – to materially improve your financial position. This could include advice to help you:

-

Save tax

-

Increase equity

-

Pay down debt

-

Use super effectively

-

Balance ‘now’ with ‘later’

-

Optimise your portfolio

Small changes in each of these areas quickly add up to a big impact on your financial future.

-

Set your direction

The road to any financial objective is going to have a series of forks along the way – two (or more) routes to get to the same destination.

A lot of our work now, as financial planners, is helping people decide which route to take.

Which sounds simple.

It’s not; often, people are completely frozen when confronted with this choice. So we’re able to apply our knowledge – of them, and of the rules – to confidently show which path is most clearly in their best interests.

-

Accountability

It’s incredibly easy to lie to ourselves, to tell ourselves that ‘we’re doing everything we can’, that ‘we’re on track’, that ‘it’ll be alright’.

Which is why it’s so helpful to have somebody beyond you keep you on track.

We know where you want to go, and we can hold you accountable to your commitment to get there. The achievement of your ideal financial life requires work, commitment, change and – some – sacrifice. Having an independent person around to help you push through is immensely powerful.

-

Organisation

“It’s all such a mess – I don’t know where to start!”

If you’ve ever said this about your finances, please know that you are not alone! Our process starts with helping people tidy up their arrangements – simplifying things as much as possible.

Then we give them a summary of what they have in a nice, simple one-pager. I’ve been surprised by just what a hit this one-pager has been for people who felt so disorganised before.

Bit of a Timeline

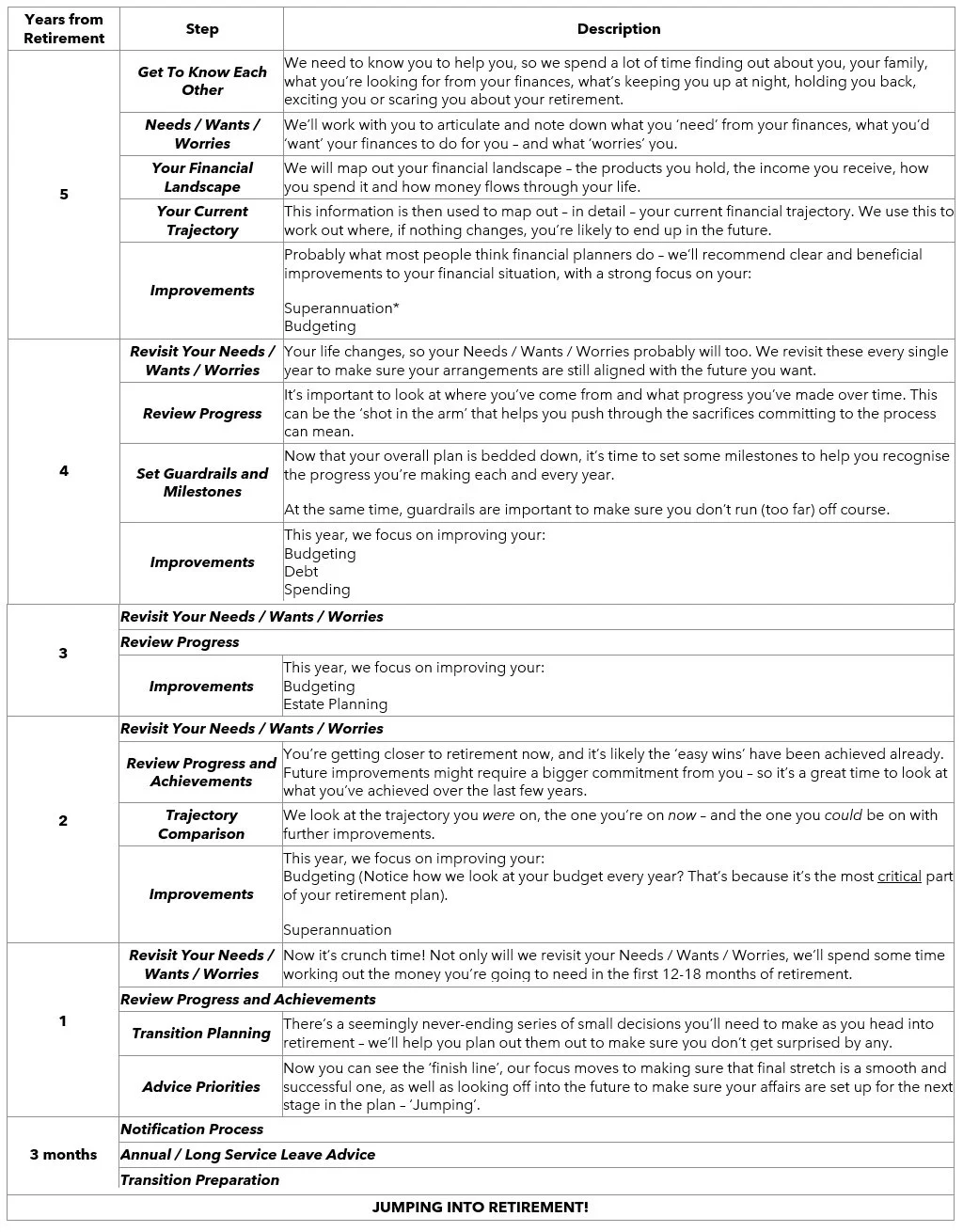

Every person’s situation is unique, so this isn’t going to be the same for everyone. But when it comes to helping somebody prepare for their retirement, our work tends to follow the same course, hopping along the same steps along the way.

Here’s a – very approximate, vague – timeline of the steps we’ll take through the Planning phase:

Advisory ‘Intensity’

Again, in a very vague way, you could expect this kind of planning and advisory process to follow this kind of a pattern – I’ve tried to capture how the intensity of the advisory process ebbs and flows over the years leading into retirement:

Intensity

Which would make sense, I think.

The first phase is quite intense – we’re getting everything back into shape and setting the priorities that give you the greatest chance of having the retirement you desire.

But in subsequent years, that intensity will dial down a little, because it becomes about letting the plan play out. Things are stilled tweaked as time passes, but it shouldn’t be about wholesale changes in this stage – it’s all about management.

Then things ramp up again in the final year before you stop working. Making sure everything is ready ups the intensity to make sure your final day at work is a joyous day, free of worries and fears about the future.

How Do You Feel?

Another thing you might like to think about – how would you feel through this process?

Would going through an intense period of financial improvement leave you feeling relieved? Organised? Or exhausted and anxious?

The overwhelming feeling we’ve seen is relief, but I’ve worked with people before who hated the process – who liked having their head in the sand. They knew they had to take these steps, but they certainly didn’t enjoy them!

Just Part One

So this is how a financial planner can help you plan for your best retirement.

This first phase of the process – the ‘Planning’ phase – is critical because it can help set you up for a wonderful retirement.

Done properly, and with enough time, the hard work you do in this stage will give you financial momentum so that journey into retirement is exciting, smooth and joyful.

Next week, I’ll outline how we help you take this journey when the time comes, before hopping into the third stage of your retirement plan – Landing.